All Categories

Featured

Nevertheless, these plans can be more complex compared to various other sorts of life insurance policy, and they aren't necessarily appropriate for each capitalist. Speaking to a knowledgeable life insurance policy agent or broker can help you determine if indexed global life insurance is an excellent fit for you. Investopedia does not offer tax obligation, investment, or economic solutions and advice.

, adding a permanent life policy to their investment profile might make feeling.

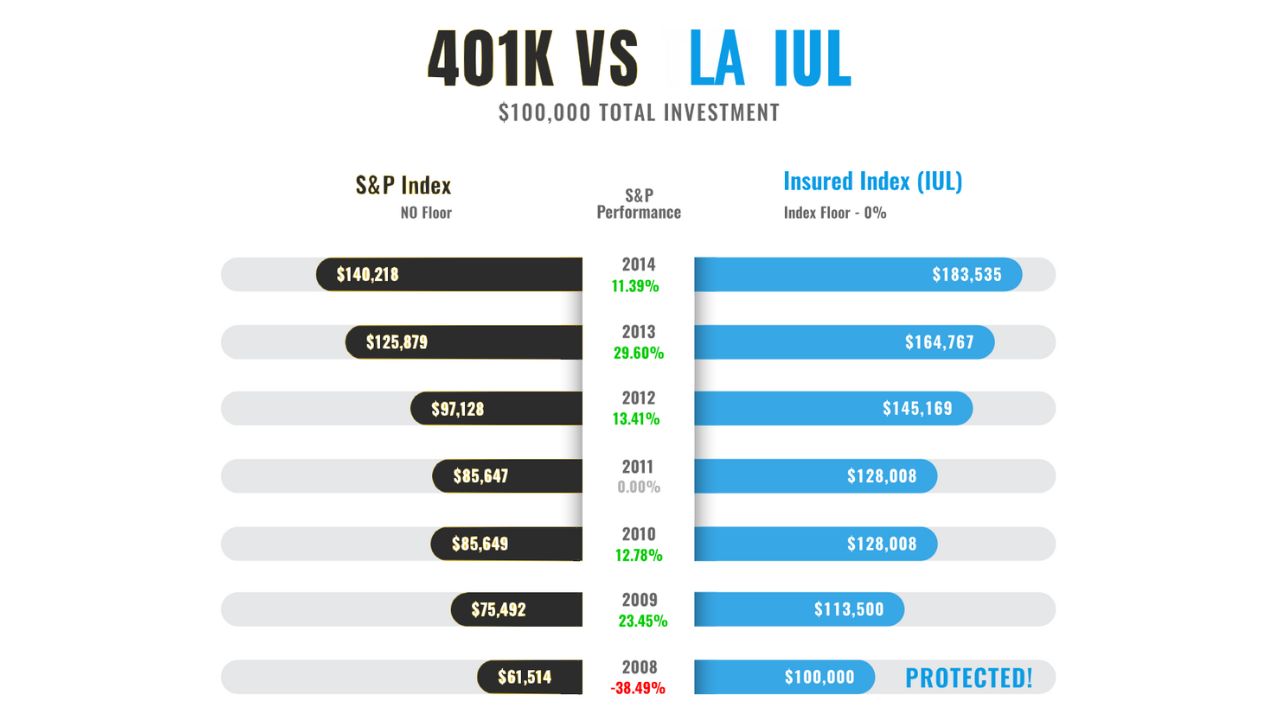

Low rates of return: Recent research study discovered that over a nine-year period, employee 401(k)s grew by approximately 15.6% per year. Compare that to a set rate of interest of 2%-3% on a long-term life plan. These distinctions accumulate over time. Applied to $50,000 in savings, the charges above would certainly equal $285 each year in a 401(k) vs.

In the very same blood vessel, you might see investment development of $7,950 a year at 15.6% passion with a 401(k) contrasted to $1,500 each year at 3% rate of interest, and you would certainly spend $855 even more on life insurance policy monthly to have whole life coverage. For most people, obtaining irreversible life insurance as part of a retirement is not an excellent concept.

Dave Ramsey On Iul

Below are 2 typical sorts of irreversible life plans that can be utilized as an LIRP. Entire life insurance policy offers fixed premiums and cash value that expands at a set rate established by the insurance company. Conventional investment accounts usually offer higher returns and even more versatility than whole life insurance policy, however whole life can supply a relatively low-risk supplement to these retired life financial savings methods, as long as you're positive you can afford the premiums for the life time of the policy or in this situation, until retirement.

{kind=link}

Latest Posts

Iul Life Insurance Vs Whole Life

Iul Benefits

My Universal Insurance